%20(3).webp)

In a market teeming with noise and performative appraisals, LPs are discerning about who to bet on long term.

The LP ecosystem is intricate and can appear opaque to those outside of it. As investors in venture funds, LPs prioritise sturdy return on investments as well as promising fund managers that can execute a strong business strategy.

In Europe, pension funds, insurance companies and family offices have played a crucial role in providing the capital necessary to bolster the continent’s technological ecosystem. And their efforts have been paying off; per a report from Invest Europe, since 2002, European VCs have snagged an annual net return of 12.65% on investments, compared to US’ investors 12.25%.

Ultimately, LPs need to feel confident that GPs are a natural fit for their portfolio — and that they can reliably deliver returns and provide the desired exposure.

Lisa Edgar, partner emeritus at Top Tier Ventures and advisor to funds such as Open Ocean, has some words of advice for fund managers. She highlighted how fund managers and GPs can clinch actual LP approval — and what to be mindful of when navigating the GP-LP dynamic.

Finding alignment

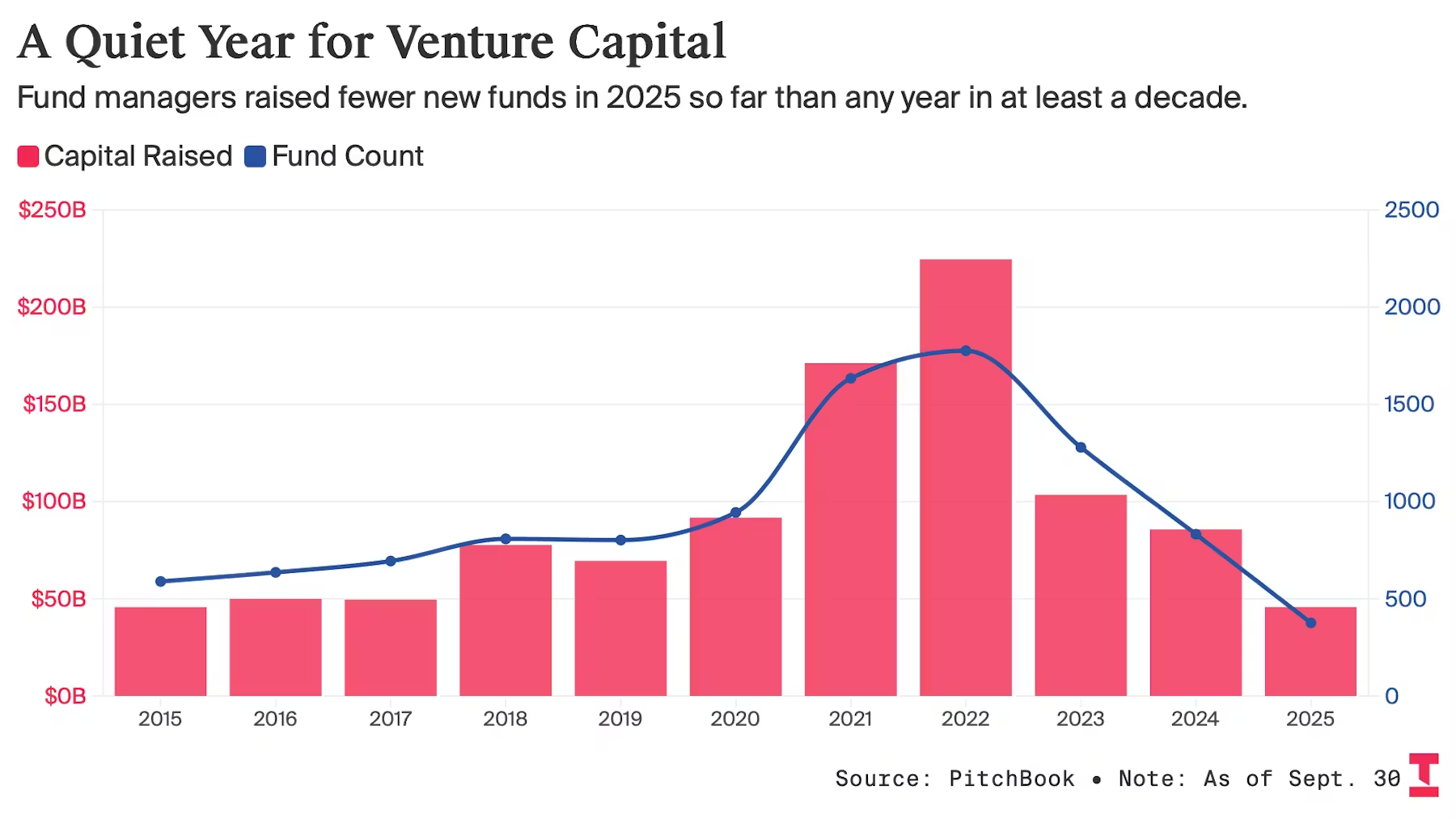

GPs can no longer take an indiscriminate and un-coordinated approach when fundraising; after all, venture capital fundraising slumped massively in 2025 amid a weakened IPO market and continuous geopolitical tensions. In 2025, fund managers raised fewer new funds than any year in the past decade, per The Information.

This is why taking an organized and laser-focused attitude to approaching LPs is key, Edgar told European Women in VC in an interview.

Alignment isn’t about convincing everyone — “it’s about finding your natural buyers,” she said. “If you’re a $40 million fund, large pension funds probably aren’t your natural fit.”

The best thing emerging managers can do is focus on who is structurally aligned with their size and strategy. Often, LPs operate under portfolio constraints, sometimes adopting a “one in, one out” approach, and so even the strongest of funds might not find a spot in their portfolio.

GPs can look inwards, Edgar said. “Think about fundraising the way entrepreneurs do: find your product-market fit.”

Navigating the LP relationship

It’s no secret that the VC ecosystem is largely relationship-driven. Established LPs source primarily through trusted networks and shared diligence. There's no central repository, no shortlist. Deals and managers surface through personal connections, word of mouth, and peer referrals.

That makes it less likely for them to reactively chase themes or buzzy sectors. Case in point, headlines have shifted from climate to defence tech to AI as the new topics de jour, but LPs aren’t willing to throw cash at any fund manager that can tout the buzz words.

It’s also important to understand that meetings don’t always equate to momentum.

“Everybody is polite and businesslike — we call that LP love,” Edgar notes. It’s equally important to “figure out how to read the LP love.”

If GPs have a meeting, and fit the LP strategy bill, they should be mindful to let the relationship organically proceed. For one, firing dozens of questions to LPs won’t always fare well and can sometimes come across as aggressive or even desperate, Edgar said.

A positive signal, post-meeting, is when LPs themselves follow up and ask for progress updates. “When someone does that, they are doing their work,” Edgar added. “They want to be able to consider an investment now or in the future, so that I would absolutely follow up on.”

The LP checklist

LPs generally have one goal: can managers produce the desired return?

“They don’t want to choose you and then something goes sideways and they have to justify the decision to their board and potentially help fix the problem,” she said. To assuage these concerns, LPs need a compelling reason as to why they should back new funds. Here, execution signals overshadow rhetoric.

Institutional capital typically takes 9-18 months to anchor; as a long-term discipline, institutional investors want to see longevity in the fund’s strategy through established performance.

It’s why time-to-close isn’t a serious red flag for experienced LPs, especially if the fund is investing during the raise, she said.

Diversification has also been top of mind for leading LPs. Over time, the trajectory of US investors backing European funds has been increasing, Edgar found.

In addition, many American LPs have found it difficult to invest in mainland China, and Europe has become a viable alternative for that capital.

Curiosity for the continent has piqued. “While they look at performance, diversification and allocation, it is also a curiosity — I see an increasing number of US investors come to various events such as Slush to try and understand what’s happening.”

And there’s much to be coveted in the European tech ecosystem. European VCs have outperformed US investors over the past decade, with 10 year returns of 20.77% compared to the 18.18% touted by American VCs, per Sifted.

A slate of mega-rounds in the likes of Lovable, Mistral, and NScale, as well as Klarna’s public listing, offer a peek into the dynamic potential of the region — for GPs and LPs alike.

Lisa Edgar an Independent Advisor and Partner Emeritus at Top Tier Capital Partners after serving as Co-Founder and Managing Director since 2003. She is a strategic advisor to OpenOcean, a London-based venture capital fund.